Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

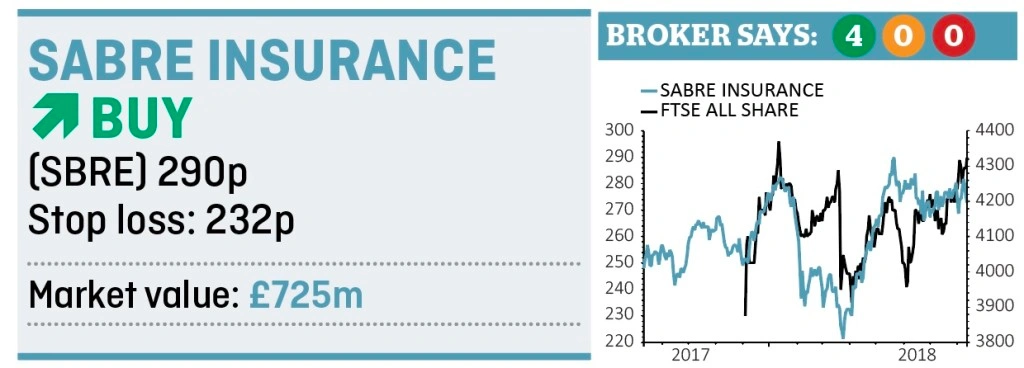

magazineLoad up on Sabre Insurance for juicy dividends with potential 7.8% yield

The market is starting to have more faith in Sabre Insurance (SBRE) so now could be a good time to snap up this generous dividend payer and highly profitable business.

Sabre floated on the stock market in December 2017 and was ticking along nicely until March this year when the share price took a hammering upon publication of its full year results.

Berenberg analyst Trevor Moss says the insurer ‘got a proper market kicking’ for failing to grow when market conditions weren’t right. ‘We thought this was a poor market reaction and still do,’ he adds.

The company has previously talked about wanting to prioritise profitability over chasing market share; however it had no choice but to cut prices earlier this year to stay competitive amid softer market conditions.

Importantly, Sabre was able to maintain its market leading combined ratio in the first half of the year despite lower premium rates, suggesting there has been an equal offset from lower claims costs.

The combined ratio is an insurance company’s measure of profitability. The lower the number, the more profitable the company’s underwriting operations.

For the six months to 30 June, the company had a combined ratio of 68.6% and pre-tax profit of £32m, a 14% improvement on the prior year.

TAKING ACTION

Chief executive Geoff Carter last month said the company took pricing action to reflect ‘observed reductions in the frequency of small claims earlier in the period under review’.

He added: ‘It is apparent that other insurers made similar adjustments, some earlier than Sabre, which meant that we lost some market share in the first few months of the year.’

In May, Moss at Berenberg insisted that Sabre should be viewed as an income stock, not a growth stock.

‘Growth is an outcome, not an aim, for Sabre with the company trading volume and price for the benefit of shareholders,’ stated the analyst. ‘While we expect this can result in growth over the medium term, it may cause some volatility as investors grow comfortable with this approach.’

THE SECRET OF SABRE’S SUCCESS

Sabre focuses on niche parts of the market, writing policies for ‘non-standard’ drivers who tend to shunned by the major insurers. These include among others, young male drivers who may drive powerful cars.

This focus allows the business to charge higher premiums than the average player although this is justified by the greater risk it is taking.

The company trades on 14.5 times 2019 forecast earnings and offers a 6.2% prospective dividend yield based on Numis estimates. Berenberg has higher dividend expectations, believing Sabre will pay 22.1p per share in 2019, equating to a 7.8% yield. (DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.