Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMore in the tank for TT Electronics as it scales value chain

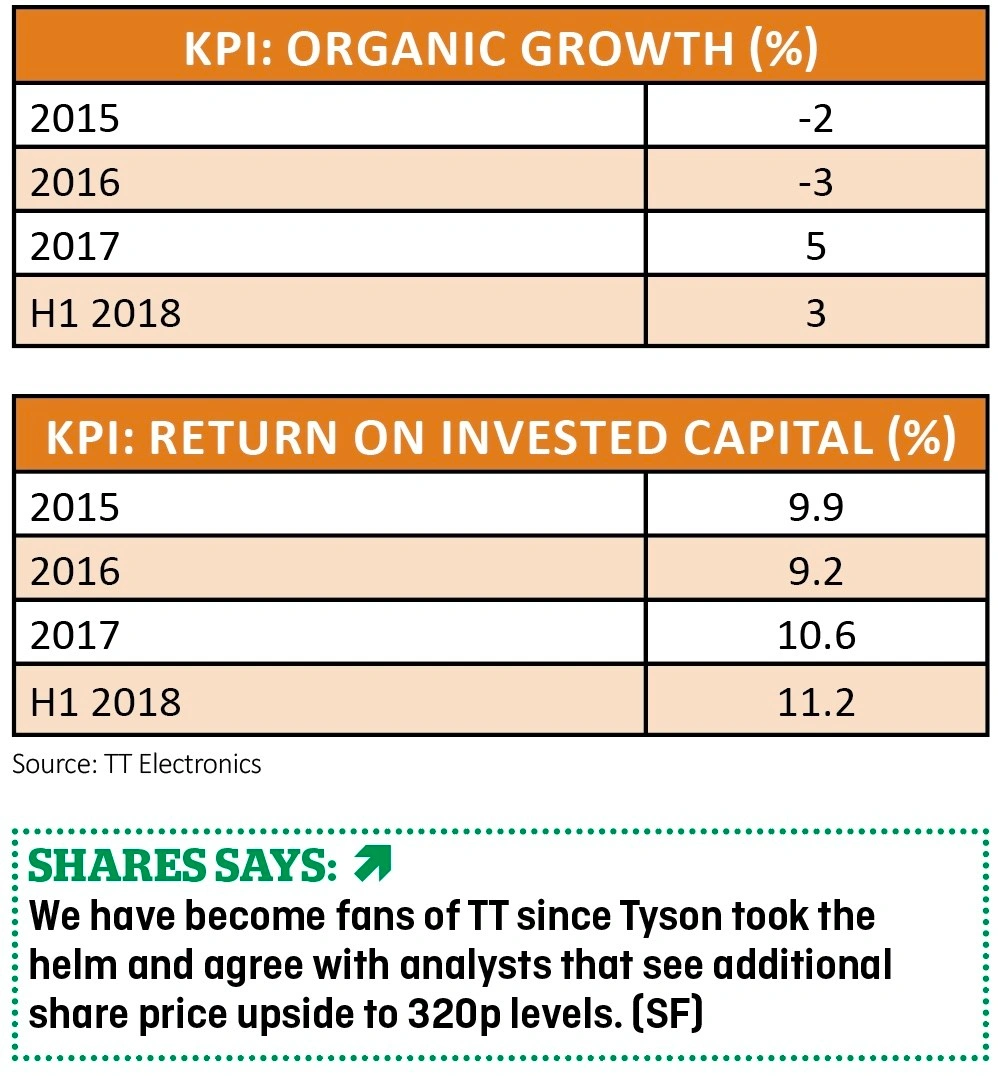

An acquisitions spree designed to drag TT Electronics (TTG) up the value chain is paying off with operating profit margins soaring beyond analyst expectations.

In half year results to 30 June the electronic components business reported profit margins of 7.5%, ‘well ahead of our 6.7% expectations,’ say analysts at Berenberg. That has prompted the investment bank to upgrade forecasts by between 8% and 10%, with profit margins ‘trending to 8.6% by 2020,’ the researchers say.

That’s exactly double the 4.3% profit margin run-rate back in 2015, when chief executive Richard Tyson joined the business.

Part of the reason for this robust performance is a telling contribution from Stadium in the UK and, to a lesser degree, US-based Precision, a pair of businesses acquired during the first half (April and June respectively).

EMBRACING THE DIGITAL AGE

These additions are helping TT expand beyond its traditional sensors and instrumentation markets into fast-growing, and importantly more profitable, digital niches. These include areas like supplying complex connectivity, automation and machine learning components and systems for automotive, industrial and medical applications, where TT is increasingly investing in in-house designed solutions.

TT management gave an upbeat assessment of the foreseeable future, with Tyson talking up ‘confidence of progress for the full year ahead of our prior expectations’. This optimism is supported by a book-to-bill ratio above 1.0, implying that the company is winning future workloads at a faster rate that it is currently producing products.

TT shares have rallied roughly 20% to the current 265p since Shares last wrote about the company on 26 April, where we highlighted the improving prospects of the company. That still leaves the stock trading on an implied 2019 price to earnings multiple of less than 15.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.