Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

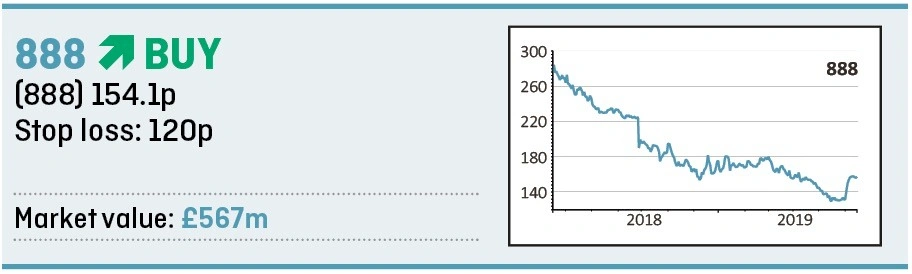

magazine888 has a plan for a sporty comeback

The tough regulatory backdrop has seen shares in the largest London-listed gambling sector names fall by an average 43% over the past 12 months. We believe investors may have overreacted and are therefore missing out on some good opportunities, one of which is online gambling specialist 888 (888) where the market hasn’t fully recognised significant changes to the way it does business.

888 has reshaped itself from a focus on high rollers and business-to-business revenue (B2B) to a mass-market player in casino and sports betting. The ambition is to become the dominant casino player and a top tier sports operator, by scaling its proprietary technology platform.

Its shares trade on 11.4 times forecast earnings for 2020 and an EV/EBITDA (enterprise value-to-earnings before interest, tax, depreciation and amortisation) ratio of 6.4. In comparison, the average of the online gambling peer group is 12.2-times and 9.7-times respectively, according to investment bank JP Morgan.

The global casino market is still fragmented with online penetration of only 6%, compared with 44% in the UK. 888 intends to scale-up its mass market offering to grab market share, leveraging its heritage brand and best-in-class technology.

What this means in practice is that the company will be able to enter new jurisdictions with speed and the flexibility to add new features. For example, utilising its unique in-house studio, the company can offer differentiated games to fill specific gaps in the market.

At a recent capital markets day, management said that its games generate 1.46 times more bets per play than third party equivalents.

According to JP Morgan analyst Ted Nyhan, and based on year-to-date numbers, 888 is seeing implied like-for-like growth of 45% in casino revenue.

The global market for sports betting is expected to grow by 7.2% over the next five years and 888 is well positioned to capture market share thanks to its end-to-end infrastructure, which allows it to be more efficient in its marketing.

The recent BetBright acquisition enables a more effective pricing strategy and personalisation. For example cost per customer acquisition has fallen by 13% since the first quarter of 2017 and 8% since the first quarter of 2018.

While the legacy poker and B2B units are expected to remain a drag on earnings for the current year, analysts then expect a full recovery in the UK and structural growth in global casino and sports betting.

Adjusted pre-tax profit is forecast to be $65m in 2019 (2018: $87m) before progressing to $73m in 2020 and $87m in 2021.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.