Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

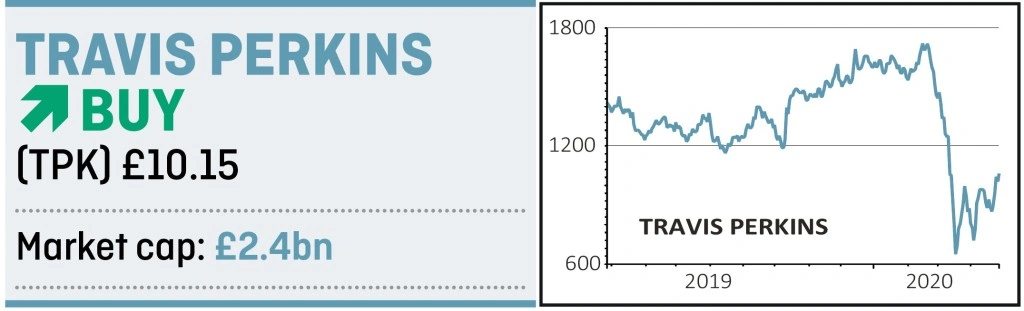

magazineTravis Perkins can capitalise on homebuilding restart

Builders’ merchants such as Travis Perkins (TPK) could be among the first businesses to return to something approaching ‘normal’ levels of activity in the next few months.

Having been shut to all but essential services since mid-March as construction work ground to a halt across the country, depots are reopening as homebuilders such as Persimmon (PSN), Taylor Wimpey (TW.) and Vistry (VTY) restart operations in the next few weeks.

The homebuilders themselves had been maintaining a low level of activity by mainly making sure partly-constructed houses were watertight and finishing those close to completion.

However, all continued to see demand for new homes meaning their contracted forward sales remain healthy, which is positive news for suppliers.

Travis Perkins came into the year with positive momentum in its core merchanting business which outperformed the market last year with 3.3% like-for-like sales growth, divided equally between price and volume increases.

Toolstation delivered an outstanding performance, increasing like-for-like revenues by 16.3% and overall sales by more than 25% due to new store openings, consolidating its market-leading position.

The TradePro and Kitchen & Bathroom units also performed well with an increased share of revenues from higher-margin installation services.

Even the consumer-facing Wickes DIY retail business, which was slated for demerger next quarter as the group wants to focus wholly on trade customers, generated close to 10% revenue growth thanks to new decorating and landscaping ranges.

Trading in the period to 20 March was in line with management forecasts, although in the first three weeks of April group revenues dropped by around two thirds.

While Government restrictions on house buying may have temporarily paused the upswing in activity which followed the general election, the market is still chronically short of new housing and indications are that demand and prices remain firm.

As well as the reactivation of the new-build sector, the repair, maintenance and installation (RMI) market should pick up later in the year as social distancing measures are relaxed.

With £125m of cash, the cancellation of the 2019 final dividend, a saving on business rates of £90m, undrawn bank facilities of £400m and no immediate funding needs, the firm’s finances are in good shape.

We would expect dividends to be restored once normal trading resumes.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Digital change expert Kainos remains a great pick

- Time to take profits on IT security group Avast

- Computacenter resilient but dividends are off the menu

- Luceco can move beyond ‘darkest hour’

- Buy ITV shares as advertising activity could soon pick up

- Travis Perkins can capitalise on homebuilding restart