Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

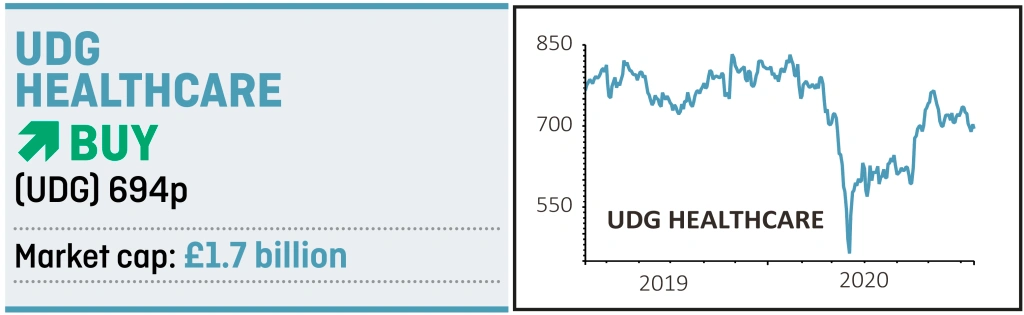

magazinePlay the healthcare boom via ‘best in class’ UDG

The global healthcare pandemic has increased awareness of diseases and the threat they pose to public health as well as economic activity. This has spurred the pace of drug discovery with an increasing number of new drugs in trials and provides a supportive backdrop for UDG Healthcare (UDG) to capture growth.

UDG provides outsourced services to over 300 healthcare companies and smaller biotech firms. It is active across the whole spectrum of health services such as helping firms bring new products to market and supporting patients to access medications.

It has two divisions: Ashfield provides advisory, communications and commercialisation services and generates just over two thirds of group operating profit, while Sharp is a leader in contract clinical trials, manufacturing and packaging.

Investment bank Berenberg estimates that roughly 20% of the company’s profits are affected by the pandemic, relating to sales reps’ work restrictions and face-to-face meetings. Sales reps have since come off the government support schemes in Belgium while Germany is showing signs of improvement and the same is expected in the UK later in the summer.

The 80% of the business not affected is showing good demand although lower expected levels of activity led the group to withdraw its earnings guidance for the rest of the year.

Low leverage will allow the company to continue deploying $100 million to $200 million on two or three acquisitions a year. Net debt-to-earnings before interest, tax, depreciation and amortisation (EBITDA) is 0.3-times.

UDG is classified by Berenberg as a ‘best in class’ company. It says such businesses can trade on higher than average valuations, but they can scale and compound high returns over many years, thus deserving a premium rating. UDG trades on 20 times forecasts earnings for 2021.

Operating profit has grown at a compound annual growth rate of 14% over the last five years. Before the pandemic management targeted underlying operating profit growth of between 5% and 10% a year with supplemental acquisitions on top.

The total addressable market across all segments is estimated to be around $30 billion a year and with UDG’s 2019 revenues of $1.3 billion implying a market share under 5%, there is plenty of runway to maintain good growth and deliver shareholder value.

‘Healthcare spending will increase as awareness in defeating diseases and combating health crises rises,’ says Berenberg. ‘Pharmaceutical companies will increasingly rely on outsourcing partners to manage complexities and improve flexibility.

‘UDG’s strong balance sheet will leave management with sufficient power to further consolidate the market. Smaller, more inefficient and more levered competitors will likely struggle over the coming months, providing UDG with opportunities to deploy capital for the right acquisitions.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Market share gains to fuel Motorpoint

- Analyst upgrades Luceco forecasts for the second time in as many months

- Play the healthcare boom via ‘best in class’ UDG

- QinetiQ growth strategy progressing despite challenges

- Buy care home investor Target Healthcare for a 6% yield

- Hipgnosis is cashed up and ready to buy more songs

- Ocado has a monumental growth opportunity

Investment Trusts

Money Matters

News

- US earnings season unlikely to add clarity to full year outlook

- Red hot Tesla could put huge stock offering on the table

- Fevertree shares fall on margin concerns

- Global company debt could jump by $1 trillion in 2020

- Halma’s record profit streak set to end

- B&M shares hit new record high as analysts upgrade forecasts