Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

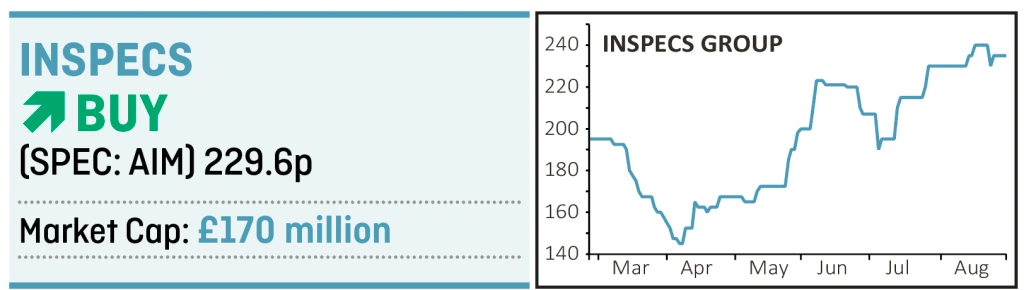

magazineWe spy an attractive growth story at Inspecs

Bath-based eye wear frame specialist Inspecs (SPEC:AIM) has compelling growth credentials which have been masked by disruption to Asian supply chains and closing of opticians during lockdown.

We believe this has created a great opportunity to buy the shares at a decent price. On 2021 earnings the shares trade on a price-to-earnings (PE) ratio of 14.8 according to estimates from broker Peel Hunt.

There is a degree of pent-up demand from customers who want or need to have their eyes tested and are more likely than before to follow through with a purchase of new frames, given the extra effort required to book appointments.

Peel Hunt believes revenue has rebounded faster than it expected earlier in the year while the business has remained cash flow positive, an encouraging sign given the operational gearing in the business.

To meet demand, Inspecs has recently expanded its Vietnamese manufacturing capacity, which increased fixed costs and held back profitability in the short-term. There is material scope over the medium-term to increase margins faster than revenue.

The global eye wear market is thought to be worth $141 billion at retail value and is expected to grow around 7% per year out to 2025 according to consultancy Statista. One of the key drivers of growth are the 2.6 billion people who currently need eye correction but not currently served, representing 57% of a total market of 4.6 billion.

Increasing prosperity and awareness of the damage caused by sunlight and blue light from computer screens are also key factors driving growth.

Clear advantages

Inspecs operates a vertically integrated business model which means it is one of the few companies in the sector to offer one-stop-shop services to its customers. It designs, manufactures and distributes both private label frames and branded products, which it sells under licence for long standing customers such as Superdry and Caterpillar.

Unusually for a small business, the company has built a broad global distribution platform with over 30,000 points of sale, selling to key customers like Specsavers and Grand Vision as well as thousands of independents and opticians.

This is a very valuable part of the business that will provide an important source of growth as the business adds new customers and brands while building scale and increasing profitability.

In our view Inspecs represents a great opportunity to get exposure to a secular growth theme. Its balance sheet position looks robust with Peel Hunt forecasting net cash of $9.4 million by the end of 2020.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Saga white knight welcomed by investors

- SDL’s tie-up with RWS offers a compelling story

- Shock resignation of Japan PM hits Nikkei

- US markets flash warning signs with echoes of past corrections

- US Federal Reserve tweaks monetary policy goals

- Beauty website owner prepares for biggest London listing of 2020