Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

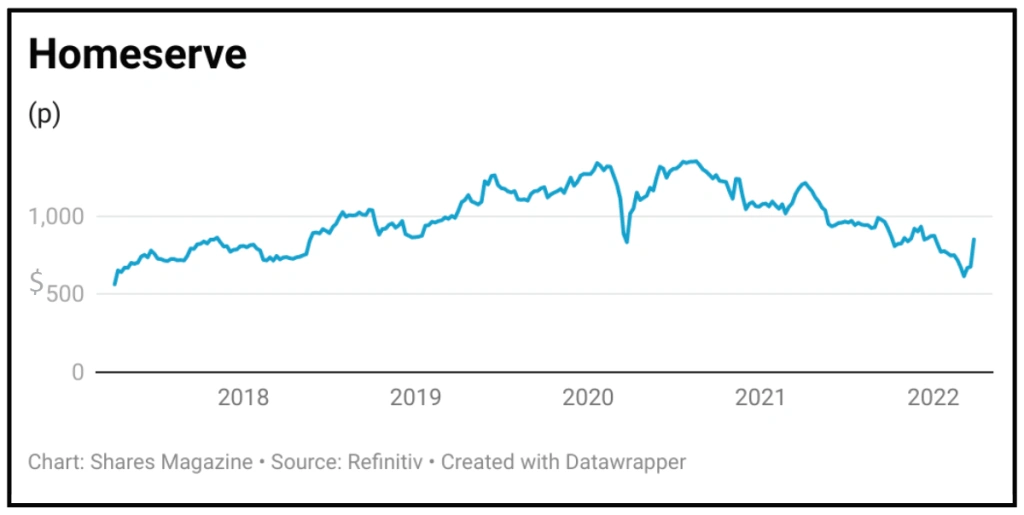

magazineHomeserve shares surge higher on bid approach

Homeserve (HSV) 880p

Gain to date: 30%

Original entry point: Buy at 675p, 24 March 2022

Just as soon as we had recommended home repair services group Homeserve (HSV) as a buy on 24 March, its shares jumped sharply following news that Brookfield was considering a possible offer for the group.

Brookfield Asset Management is one of the world’s largest alternative investors with $688 billion of assets under management.

There are a number of factors that make HomeServe a natural target for private equity ownership. These include its inflation-protected, annuity-like income streams. Specifically the defensive and recurring nature of its revenue enables it to support higher levels of debt.

A recent industry transaction, whereby American Water disposed of its US Homeowner Services Group, suggests there could be further upside in Homeserve’s share price.

The sale in 2021 for $1.27 billion, equated to enterprise value per customer of $850, and an EV to EBITDA (enterprise value to earnings before interest, tax, depreciation and amortisation) multiple of 15 times.

Using this same EV to EBITDA multiple it would imply a Homeserve share price of £10. Alternatively using the $850 value per customer generates a value of £14.50.

SHARES SAYS: Sit tight and see how the bid situation plays out.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Make the most of your ISA allowance: three stocks to buy now

- Recession fears: How to protect and grow your wealth if the economy weakens

- How bond fund managers analyse investments and assess risk

- How important are commodities in the Brazilian economy and market?

- Emerging markets: Views from the experts

Great Ideas

- ConvaTec has turned a corner and offers growth and re-rating potential

- AG Barr fizzes to profit ahead of pre-Covid levels

- SDI’s £7.7 million deal to immediately boost earnings

- Homeserve shares surge higher on bid approach

- Value specialist Temple Bar is well placed for inflation and rising rates

- Beat inflation with Diversified Energy’s big dividends

- Strong demand drives gains in logistics, residential and development

- Our faith in the managers is undiminished despite a slow first half

Investment Trusts

News

- What a harsh EU clampdown means for Apple, Google and other big tech firms

- Why Pendragon might be the next auto retail takeover target

- US Treasury yields surge as Fed toughens stance on mounting inflation

- Mark Barnett makes a comeback with new Tellworth equity income fund

- Terry Smith uses Fundsmith investor meeting to criticise Unilever top brass