Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSaudi stake-building is no answer to BT’s dismal stock performance

The Saudi-backed Public Investment Fund (PIF) is thought to be quietly building a stake in UK telecoms giant BT (BT.A), but hopes that the sovereign wealth fund is laying the foundations for an all-out takeover have been shot down.

Rumours have emerged that PIF has been buying slugs of BT stock, although the stake remains below the 3% of the company mark which would mean having to announce details to the market.

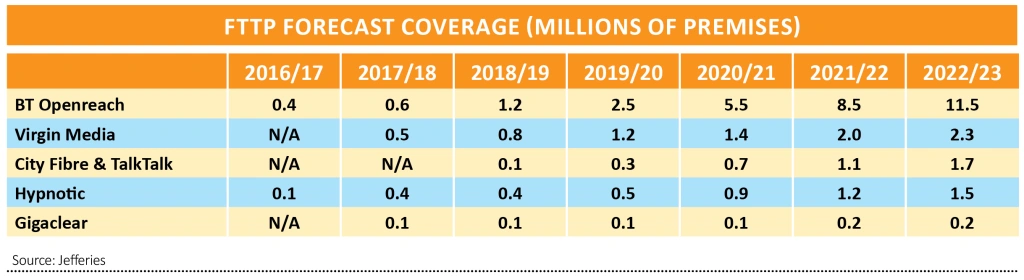

The sovereign wealth fund is also believed to have offered BT substantial new funding lines to help pay for its huge fibre to the premises (FTTP) network investment, which was apparently declined.

Broker Jefferies believes that the funding offer does illustrate a growing view that Openreach will be the only national fixed line network ‘there will ever be’, and that the ‘wall of money’ from private equity to fund rival networks is drying up.

Yet Numis, another broker, says PIF’s move is likely to have little long-term impact on the BT share price. ‘News of this investor, or any other, buying a minority stake in the telco giant is

unlikely to help its share price for more than an insignificant amount of time,’ it said.

FIBRE FUNDING MUST PROVE ITS WORTH

Numis analysts believe BT needs to back up terms like ‘value-enhancing’ and ‘value-creating’ it uses to describe the potential benefits of its big long-term spend in FTTP and to modernise itself with explicit guidance for its current five-year plan.

‘Investors appear to see extra fibre investment currently as little more than extra cost,’ said Numis’ telecoms analyst John Karidis.

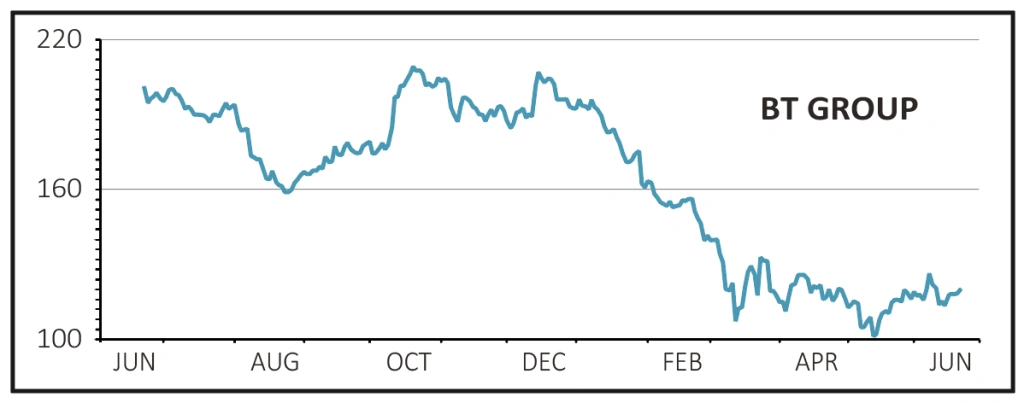

BT’s share price has fallen nearly 38% since the start of 2020, but the stock’s dismal performance has been going on for years, having lost more than 75% of its value since November 2015.

‘The stock is down 54% since chairman Jan du Plessis took office in November 2017, 50% lower since he said the share price will look after itself if BT executes the right strategy (May 2018),’ said Karidis.

He remains hopeful that a clearer earnings steer will come as Openreach and major customers reach long-term agreements on fibre network pricing and volume.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago