Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEye-catching growth in sight for Inspecs

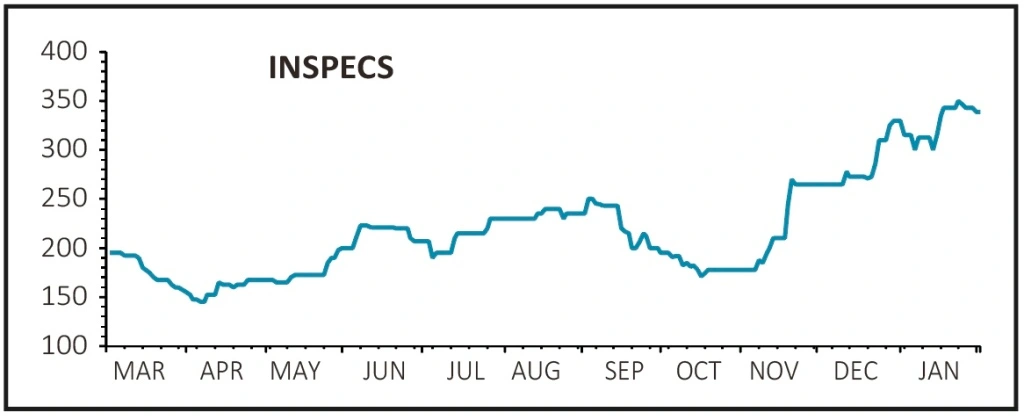

Inspecs (SPEC:AIM) 340p

Gain to date: 25.5%

Original entry point: Buy at 271p, 23 December 2020

Shares in eyewear frames designer-to-optically advanced spectacle lenses maker Inspecs (SPEC:AIM) are up an eye-catching 25.5% since we highlighted the group’s global growth potential and the scale benefits arising from the acquisition of eyewear supplier Eschenbach in December.

An in-line update (29 Jan) for 2020 showed sales coming in at $46.2 million (2019: $61.2 million), a shade ahead of Peel Hunt’s $45 million forecast, and Inspecs also flagged a good start with the integration of Germany-headquartered Eschenbach.

While Covid-related restrictions may hold back Inspecs’ short-term progress, the essential status of opticians means the eyewear industry should remain resilient during the remainder of the pandemic.

‘Inspecs is well placed to make strong progress when restrictions ease and the synergies start to come through, and now has a platform to build a materially larger business,’ says Peel Hunt.

The broker forecasts a sales surge to $241 million in 2021 for adjusted pre-tax profits of $19.5 million, ahead of $256.5 million sales and $24.9 million of taxable profits in 2022. The broker has upgraded its price target from 325p to 365p and reiterated its ‘buy’ rating on the stock.

SHARES SAYS: Keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Money Matters

News

- Amazon drops a bombshell during bumper US earnings season

- Pfizer sales boost puts vaccine economics under the spotlight

- Dr. Martens and Moonpig ‘pop’ on market debuts

- BP’s big challenge in funding its transition to renewable energy

- GameStop loses momentum but is the Reddit movement here to stay?

- What you need to know about changes to Bankers and Baillie Gifford European shares

- Marston’s fights takeover interest from US private equity firm