Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Trainline still faces a big test despite ticket commission win

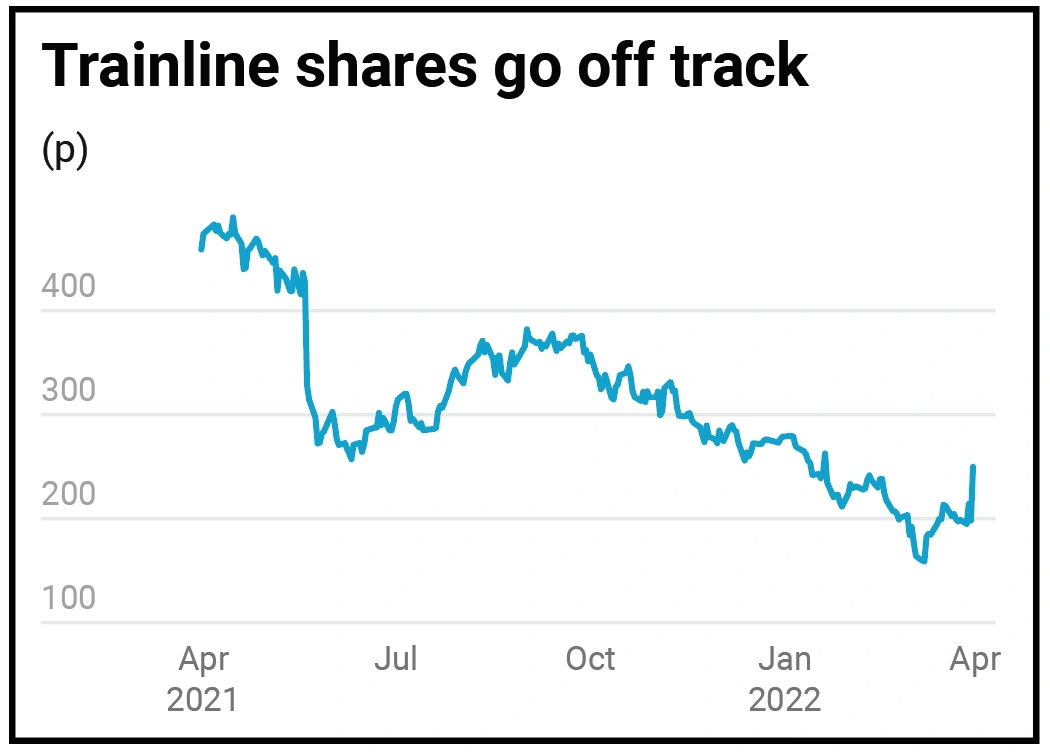

Rail ticket site Trainline (TRN) may have cleared a significant hurdle on 31 March with the news that it may only see a modest cut to the commission it derives from ticket sales but there is still one big unknown coming down the track which could knock it off course.

Its shares jumped nearly 25% on news that a proposed third-party licence deal with the new state-backed Great British Railways would reduce its commission by half a percentage point to 4.5%. A quarter of a percentage point would be offset by the removal of central industry costs.

At the current 246.5p Trainline is still 30% below the 350p price at which it floated in 2019. The pandemic hasn’t helped but market sentiment has also been soured of late by the May 2021 launch of GBR and the news it will become a central hub to sell train tickets online which poses a significant threat to Trainline’s market share.

Much will rest on whether Trainline is chosen to provide white label services to GBR in the same way it currently does to various train operators for their own sites. The tender commenced on 1 April and is expected to run for six months.

Winning this tender would provide some protection to Trainline’s business, though it would likely result in a hit to profitability if its own site experiences reduced transaction volumes and therefore reduced commission.

Even worse is a scenario in which GBR chooses another partner or takes the whole process in-house. It seems likely that as a government body, tickets sold through the GBR site would be cheaper as they could well be sold free of any commission.

Trainline is an established brand and may offer some innovative features, like flagging cost savings through splitting your journey into multiple tickets that cost less in total than one ticket for the whole route.

However, a new official ticketing site from GBR, likely to be heavily publicised and potentially offering cheaper fares, will test rail users’ loyalty to Trainline to the limit.

Liberum analyst Ciaran Donnelly remains convinced that, assuming the rail operators stop selling tickets themselves and consumers are faced with a straight choice between GBR and Trainline, the latter will prevail.

Donnelly says: ‘The most powerful defence any online platform has is its consumer relationship. It is the most difficult aspect to disintermediate, and we have seen challenger brands try to compete in other markets unsuccessfully, such as Rightmove (RMV) and Auto Trader (AUTO).

‘Similarly, Trainline has extensive experience competing in this space and has built and retained its market leading position.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Invest with confidence - four funds which make a perfect portfolio

- European shares tend to do well when the US raises interest rates... not this time?

- Why Trainline still faces a big test despite ticket commission win

- Our 2022 stock portfolio rises against a volatile market backdrop

- ESG investing faces a watershed after Russia’s invasion of Ukraine

Great Ideas

- Euromoney set to benefit from strong growth as data-driven businesses excite

- Zoo Digital sets up shop in Scandi-thriller homeland after Bollywood move

- Invest in Rathbones as a wealth management bid frenzy highlights value appeal

- Soaring book sales help publisher Bloomsbury beat sales and profit expectations

- Casual dining group The Fulham Shore offers great scope for growth

- Belvoir continues to enjoy strong tailwinds in the UK property market