Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePrivate equity has made a lot of people rich – how do you get invest in it?

Listing shares on a stock market used to be the default option for many businesses, providing them with access to a large pool of investors to tap up for funding and the ability to use their shares to pay for acquisitions.

However, private equity funding now provides many businesses with a lot of the benefits of a public listing but without all the hassle.

Even though an increasing number of businesses are shunning the stock market, retail investors can still get exposure to privately-owned companies. The simplest way is to buy shares in a private equity-focused investment trust or exchange-traded fund. These funds invest directly or indirectly in private businesses.

The activities of private equity come under three broad categories:

1.Buyouts: This is where a private equity takes a controlling stake or outright ownership of a business with the intention of helping the company grow profit. Typically, after three to five years, the private equity group would seek an exit either through a trade sale or an IPO. The latter stands for initial public offering, and which is the first chance for the public to directly own shares in a business via the stock market.

2.Venture Capital: A form of financing that private equity firms provide to young companies and small businesses that are believed to have long-term growth potential. The investor will also provide advice on using capital markets to raise finance in the future.

3.Growth capital: A private equity firm will make a minority investment in a more developed company. The capital is used to enable the company to expand or restructure operations, enter new markets, or finance a significant acquisition without a change of control.

BENEFITS OF STAYING PRIVATE

So why are more companies staying private for longer? Private companies can avoid the scrutiny of semi-annual reporting, and the associated media and investor scrutiny that comes with being listed on the stock market. Moreover, by remaining private, a company can retain more control over its ownership and ensure finances and strategies remain confidential.

For investors it is important to acknowledge that increasingly the real value and growth is often created at an earlier stage in a company’s lifecycle.

Invariably this is when companies are private. In many instances, companies come to the public market after private equity investors have made their money and are looking to cash out.

WHAT IS PRIVATE EQUITY?

In a nutshell, private equity involves investing in companies that are not listed on the public equity market. These are often referred to as unquoted or unlisted companies.

Private equity investments typically aim to create value in businesses by financing growth, operational improvements, and other changes.

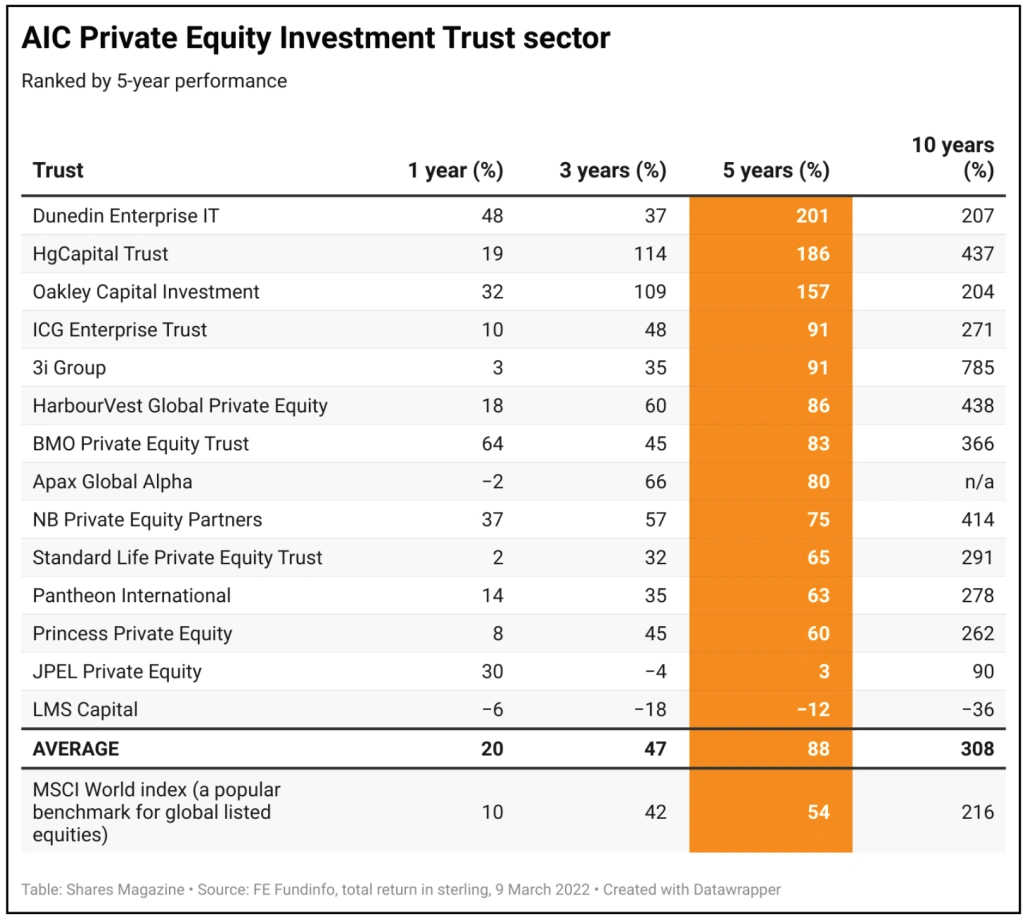

HOW MUCH MONEY COULD YOU HAVE MADE?

The average return from 14 investment trusts in the AIC’s private equity sector over the past 10 years is 308%, factoring in both share price gains and dividends. That compares to a 216% return from the MSCI World index which is a popular benchmark for global listed equities.

This outperformance can also be seen on a five, three and even one-year basis.

While there are no guarantees that private equity will continue to deliver superior returns, the past performance data does highlight the attractions of this part of the investment universe.

RISKS TO CONSIDER WITH PRIVATE EQUITY INVESTING.

Before you make the step and invest in a private equity-themed fund or investment trust, there are four main areas of potential concern to consider.

The first is the fact that investments in private companies are illiquid. It can take time for a private-equity investor to sell their holding in an unquoted business as they’ve got to actively seek a buyer. They can’t simply sell the shares on the market, which is what a fund manager would do if they invested in quoted equities.

Valuation is another issue. Valuations of unquoted holdings are often updated only once a quarter, so there is a lack of immediate transparency that investors have with companies which trade on a stock market.

Private equity often involves the use of debt to acquire companies and the investee companies may have borrowings. Given that we are in a rising interest rate environment, debt is a potential area of concern.

Another risk associated with private equity is that charges can be high and performance fees are often levied. Conversely, public equities can be accessed at lower cost levels.

However, it is important to recognise that private equity can be a high returning asset class. Arguably the associated fees are a necessary pre-requisite to access these potential returns.

THE ETF ROUTE

For investors looking to gain exposure to the private equity sector, there exists an exchange-traded fund called LPX Private Equity Swap (XLPE) which tracks a basket of private equity companies including EQT, Blackstone and KKR.

These three companies account for 34.6% of the portfolio, so there is concentration risk – i.e. if someone goes wrong with one or more of these three companies it will have a notable impact on the ETF’s performance.

The ETF charges a fee of 0.7% a year. Over the past 10 years, it has delivered 15% annualised returns according to Morningstar. However, performance year to date has been disappointing, with a 17.8% decline to 9 March. This illustrates how private equity can be a volatile investment.

THE INVESTMENT TRUST ROUTE

Alternatively, investors can get exposure via private equity investment trusts, which tend to fall into one of three categories.

You have trusts which hold direct investments in private companies such as 3i (III) which has a big stake in European retailer Action.

There are also trusts which fall under the category of ‘growth capital’, namely where they provide money to help already-established businesses to scale up in exchange for a stake in the company. A good example is Chrysalis Investments (CHRY) which invests in buy now, pay later group Klarna.

And then you have private equity fund of funds. These are private equity investment trusts which invest in other private equity funds. You should get much greater diversification through these products than the other two types of private equity trusts. Examples include Pantheon International (PIN) and HarbourVest Global Private Equity (HVPE).

PANTHEON INTERNATIONAL AND HARBOURVEST GLOBAL PRIVATE EQUITY

Approximately half of Pantheon’s portfolio is invested in the US, 28% in Europe and 11% in Asia and emerging markets. In addition to its investments in funds, Pantheon directly finances companies, alongside some of its best private equity managers. Moreover, it participates directly in the secondary market (buying companies from other investors, often at a discount).

HarbourVest Private Equity also spreads its interests far and wide. Managing director Richard Hickman says: ‘HarbourVest Private Equity is well diversified; we have exposure across the whole range, from early-stage venture investments, through growth equity buyouts of all different sizes. We also have real assets including infrastructure and a small amount of credit which is the floating rate debt in private companies.’

Pantheon has delivered a 278% total return over the past 10 years, yet its shares currently trade at a 29% discount to net asset value. In a similar boat is HarbourVest which trades on a 28% discount to NAV despite generating 438% total return over 10 years.

Large discounts are commonplace among many private equity trusts, particularly ones in the fund of funds category. That can be explained by them being less transparent, a greater amount of illiquid underlying holdings and uncertainty over the true valuation of the assets.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Why Magners maker C&C can cope with unprecedented cost inflation

- Fighting cyber attacks: Invest in the world's digital defenders

- Which is better - high yield today or dividend growth tomorrow?

- New world order: the big impact of a geopolitical earthquake

- Private equity has made a lot of people rich – how do you get invest in it?

Great Ideas

- BlackRock Throgmorton is a great fund for a small cap recovery rally

- Cordiant Global Infrastructure remains a way to play the growth in digital assets

- Why Berkshire Hathaway is hitting fresh highs

- FDM shows substantial recovery potential at shares rally 21% in two weeks

- US growth can drive undervalued Homeserve shares higher

- Essentra to become a streamlined components champion

News

- Chancellor Sunak’s spring statement full of surprise support measures

- Ferguson to leave the FTSE 100 in May as it focuses on the US

- Robust results from Nike as direct to consumer strategy delivers

- IG and Plus500 venture overseas with mixed success

- Hospitality enjoys good times despite spending pressures

- Value and inflation protection leave FTSE 100 well placed

- Hong Kong suspends shares in Chinese property giant Evergrande