Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat not to do as the tax year end looms

Sticking with cash in a high inflation world

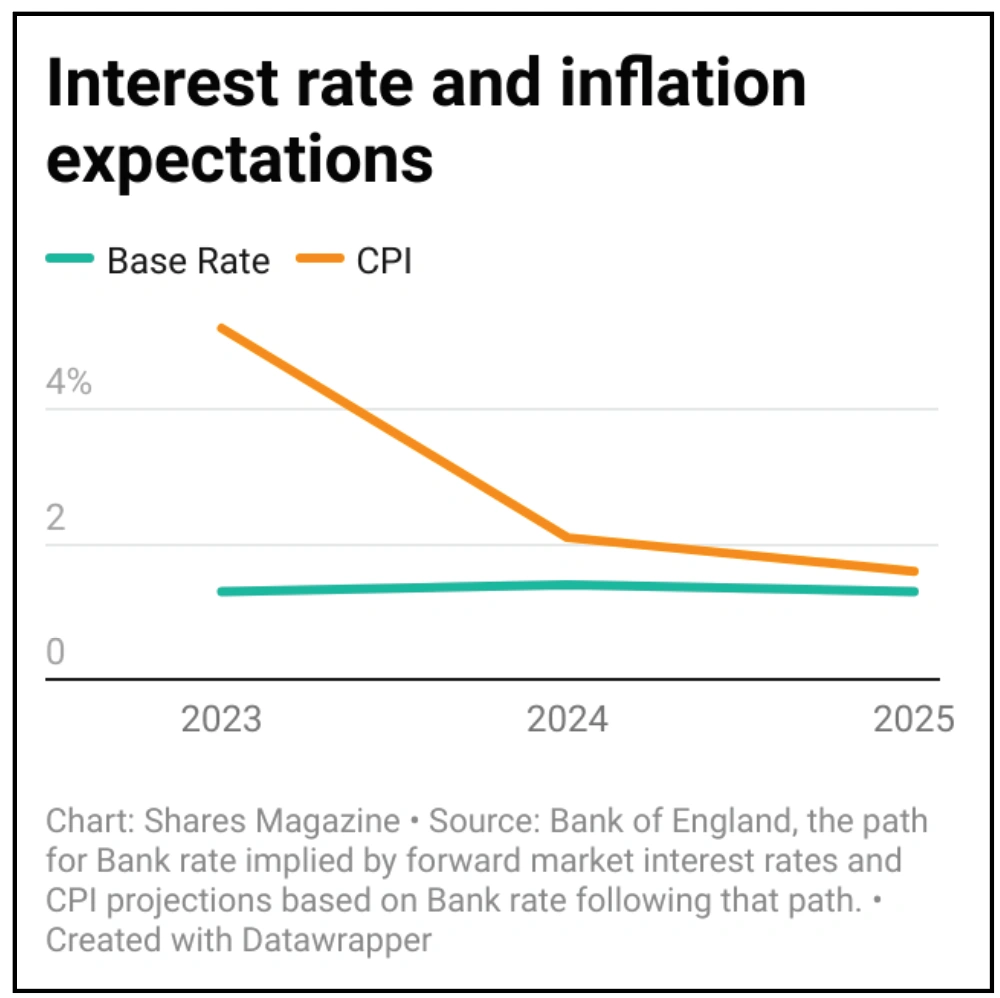

Inflation is expected to peak at more than 7% in April, just as ISA season comes to a close. Fears of savings being eaten away by inflation is probably near the top of investors’ list of worries right now. Inflation is the enemy of cash, as no cash ISA account interest rate comes anywhere near the current rate of inflation, let alone what it’s going to peak at this year.

For example, £10,000 saved in a cash account 10 years ago would now be worth just £9,385 today, after inflation is taken into account. But in the next 12 months alone, Cash ISA savers face a similar loss in buying power to the one they have experienced over the last decade. £10,000 saved into the average Cash ISA today could be worth just £9,600 this time next year, based on the latest Bank of England forecasts for interest rates and inflation, and the current margin between base rate and ISA rates (see chart, next page).

That means that you should only have your essential, short-term money in cash. While cash is a great place for short-term savings or money you need quick access to, it’s not ideal for long-term savings.

So, work out what you need in the next five years or as an emergency pot, and see how that stacks up against the amount you’ve got in cash. If you’ve got more than that set aside, think about investing it to generate a potentially higher return.

If you saved £200 a month into a cash ISA, earning the current average ISA interest rate of 0.19% you’d have a pot worth £24,250 after 10 years.

But if you invested that and earned 5% returns a year you’d have almost £31,700 – £7,444 more. Of course, there is no guarantee that an investment in the stock market will beat inflation, but over the longer term, investing in stocks is one of the key defence’s savers have against rising prices.

Not automatically reinvesting your dividend income

Any dividends from investments in your ISA can be withdrawn tax-free, but if you don’t need the income now you could use them to turbo-charge your returns. If you reinvest them you can buy more shares in the same investment, which can have a dramatic impact on the size of your ISA fund over the long term.

This is because when you buy more shares each time you receive a dividend, you then receive more dividends next time there is a pay-out, which can then be reinvested again and so on. Some investment platforms allow you to set this up to happen automatically.

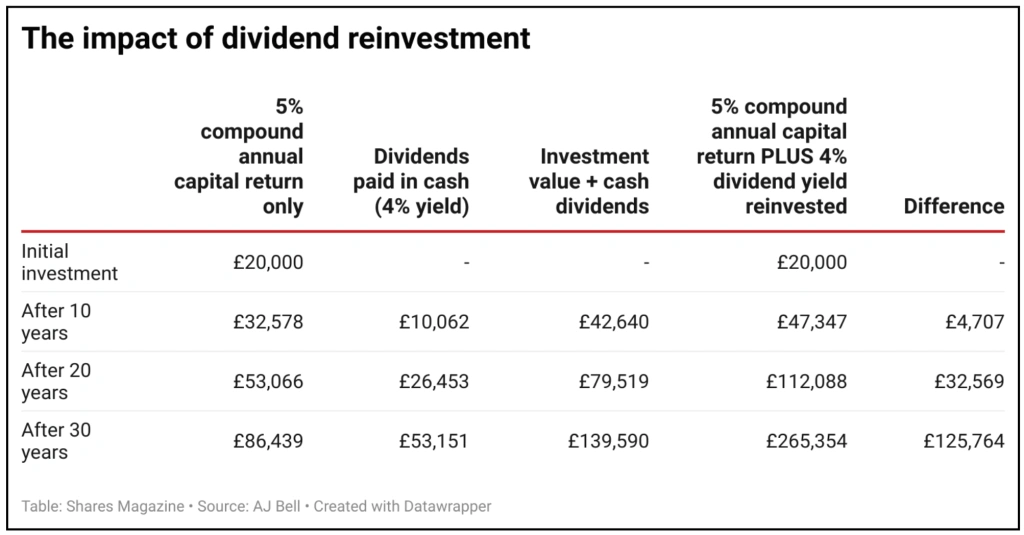

Let’s assume someone invests the full ISA allowance of £20,000 and we assume a compound annual growth rate of 5% and annual dividend yield of 4% a year. The initial £20,000 will be worth £53,066 after 20 years, and on top of that £26,453 would also have been banked in cash dividends, to give a total return of £79,519. However, an investor who reinvests the dividends rather than banking them would have £112,088 – more than £32,500 extra. The figures become even more attractive over longer periods.

Getting caught in a tax trap

The tax-free personal allowance for most people is currently £12,570. When your taxable income reaches £100,000, your personal allowance is cut by £1 for every £2 of your income, which means you lose it completely once your income reaches £125,140.

For example, someone who gets a pay-rise from £100,000 to £110,000 will lose £5,000 of their personal allowance. They will be taxed at the normal 40% income tax on their pay rise, amounting to £4,000, and then taxed at 40% on their lost personal allowance, amounting to £2,000. This means they pay £6,000 on the £10,000 pay rise – an effective tax rate of 60%.

If you are in this position you could consider reducing your taxable income so that it falls below the £100,000 level where the personal allowance starts to be eroded. Two ways you can do this are by making charity donations or contributing to a pension if you have pension annual allowance available. By contributing to a pension you are making tax savings in the form of getting your personal allowance back while also saving for your future and benefiting from pension tax relief at 40%, so you wipe out the 60% effective tax rate completely.

In a similar way as above, people will start to lose their child benefit when one half of the couple earns more than £50,000 – and the benefit will be wiped out entirely when they hit £60,000. A parent with two children will get £1,828 a year in child benefit in 2021/22 (£1,885 in 2022/23), but for every £1,000 they earn over £50,000 they will lose 10% of their child benefit – so someone earning £51,000 will lose £183.

However, parents who have just tipped over the threshold can get around this by increasing their pension contributions. What’s counted for the purposes of the child benefit ‘High Income Charge’ is your salary after any pension deductions. This means if you contribute enough to your pension to get your salary back to £49,999 then you’ll get the full child benefit again.

Forgetting about the kids

Between them a family of four can now put £116,000 in tax-free accounts in the month of April. Each adult has a £20,000 annual ISA limit and the Junior ISA limit is a whopping £9,000 now. If all four family members maxed out their allowance in early April and then again in the new tax year, they’d protect £116,000 from tax. What’s more, a weird loophole means that if your child is 16 or 17 they get the full adult ISA allowance, just for a cash ISA, as well as the Junior ISA allowance. So with one 16 or 17-year-old as part of the family your limit gets bumped to £156,000.

Now, clearly not many families have £156,000 stuffed down the back of the sofa. But it’s important to remember everyone’s ISA allowances and to also put money away for your children if you have spare cash. If you put money into a Junior ISA your children won’t be able to access the money until they are 18, at which point it automatically turns into a normal ISA and transfers into their name, giving them full access.

If you contribute the maximum £9,000 each year from birth and achieved a 5% investment return after charges each year, the pot would be worth almost £266,000 by the time your child turns 18. Even a more modest £50 a month, earning 5% returns a year, would give your child a £16,000 present on their 18th birthday.

If your child is a bit older you don’t need to feel like you’ve missed the boat. Even if you don’t start saving until the age of 10 and you put away £50 a month then you’d have built up a pot worth almost £7,000 when they hit 18. If you increased that contribution to £150 a month then you’d have £20,850.

DISCLAIMER: Financial services company AJ Bell referenced in this article owns Shares magazine. The author of this article (Laura Suter) and the editor (Tom Sieber) own shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Why Magners maker C&C can cope with unprecedented cost inflation

- Fighting cyber attacks: Invest in the world's digital defenders

- Which is better - high yield today or dividend growth tomorrow?

- New world order: the big impact of a geopolitical earthquake

- Private equity has made a lot of people rich – how do you get invest in it?

Great Ideas

- BlackRock Throgmorton is a great fund for a small cap recovery rally

- Cordiant Global Infrastructure remains a way to play the growth in digital assets

- Why Berkshire Hathaway is hitting fresh highs

- FDM shows substantial recovery potential at shares rally 21% in two weeks

- US growth can drive undervalued Homeserve shares higher

- Essentra to become a streamlined components champion

News

- Chancellor Sunak’s spring statement full of surprise support measures

- Ferguson to leave the FTSE 100 in May as it focuses on the US

- Robust results from Nike as direct to consumer strategy delivers

- IG and Plus500 venture overseas with mixed success

- Hospitality enjoys good times despite spending pressures

- Value and inflation protection leave FTSE 100 well placed

- Hong Kong suspends shares in Chinese property giant Evergrande